Understanding Credit Score Europe

If you’ve ever wondered “How to improve credit rating in Europe?” or searched “credit score Europe,” you’re not alone. Unlike in the United States, where most people rely on a centralized FICO or VantageScore system, Europe’s credit landscape is highly diverse and often misunderstood. In many European nations, there’s no single, unified credit score that follows you across borders. Instead, each country operates its own system or uses credit history differently when assessing your financial trustworthiness.

This deep‑dive article will guide you through 7 proven steps to achieve a perfect credit score fast in 2026‑2027, blending EURO‑wide strategies with practical tips that work regardless of where you live in Europe.

By the end of this comprehensive guide, you’ll understand how these systems work, how lenders view creditworthiness, and actionable steps you can take to boost your credit rating and access better financial opportunities.

What Does “Credit Score” Mean in Europe?

Before we get into steps, let’s clarify:

- Europe does not have a single universal credit score. Each country may use different reporting systems and agencies.

- In some countries like Germany, Spain, or Italy, private credit bureaus compile credit information that lenders use.

- In others like the UK, multiple agencies give a numerical score based on payment history and credit behavior.

Despite the differences, common factors influence creditworthiness across Europe — payment history, debt levels, errors on reports, and account behavior are universal themes we’ll explore below.

Step 1: Know Your Current Credit Standing

You can’t improve what you don’t measure — this is the foundation of how to get a perfect credit score in Europe.

- Get your latest credit report

- In nations with established bureaus (e.g., UK’s Experian, Equifax, TransUnion), you can access your credit report directly.

- In other regions, information may reside with local banking associations or bureaus like Germany’s SCHUFA.

- Check for errors and discrepancies

Many credit reports contain mistakes — outdated addresses, incorrect debt listings, or duplicate entries.

Pro tip: Under EU GDPR data protection laws, you often have the right to request and correct any incorrect credit data at least once per year. Doing this can boost your credit assessment quickly.

Step 2: Understand the Factors That Impact Your Score

Unlike the U.S., European lenders don’t only look at one number — they assess creditworthiness holistically.

Here’s a quick breakdown:

Credit Elements That Matter Most

| Factor | Why It Matters | How It Helps You |

|---|---|---|

| Payment History | Indicates reliability | Timely payments boost trust |

| Debt Level & Utilization | Too much debt signals risk | Lower balances improve perception |

| Credit Report Accuracy | Mistakes can harm your rating | Corrections remove unjust penalties |

| Length of History | Older, stable accounts signal responsibility | Longer history improves credit trust |

| Hard vs Soft Inquiries | Too many credit applications look risky | Fewer hard pulls preserve credit health |

This table summarizes general patterns lenders use, even though exact scoring algorithms vary by country and institution.

Step 3: Pay On Time — Always

This is THE most critical credit factor almost everywhere.

- Making payments on schedule signals lower risk to lenders.

- Missed or late payments stay on your file for years and damage your credit rating.

Tips to pay on time:

- Set automated payments for bills.

- Use calendar reminders for due dates.

- Prioritize clearing credit card balances before interest accrues.

Step 4: Manage Your Debt Smartly

Your overall debt and how you use it influences how lenders view your financial health.

Key Insights:

- Keep high‑interest debts paid down first.

- Avoid maxing out credit lines — a utilization over 30% can raise red flags.

- If possible, negotiate with lenders to reduce interest or extend payment terms.

Why this matters: Even if a nation doesn’t use a numerical score, lenders look at how responsibly you manage existing credit before offering new loans or products.

Step 5: Maintain Financial Stability

Stability isn’t just about credit behavior — it’s about your financial lifestyle.

✔ Stay at a consistent address if possible — frequent moves can signal instability.

✔ Keep long‑term accounts active — older accounts often contribute positively.

✔ Avoid excessive new credit applications in short bursts — this signals risk and can lower your standing.

Step 6: Build a Positive Payment History Across Accounts

Even though Europe doesn’t universally track all credit in one number, showing “responsible financial behavior” is powerful.

There are emerging services and tools such as Experian Boost that allow you to include regular bill payments (like utilities, streaming service subscriptions, council tax) in your credit evaluation.

This step helps especially if you:

- Have a thin credit file

- Are new to credit

- Want to show diverse positive financial behavior

Step 7: Use Best Credit Score Hacks for Europeans

Here’s where strategy turns into results

Smart Hacks

- GDPR Requests: Use your data rights to eliminate errors or outdated marks.

- Soft Credit Searches: When shopping for credit, ask for “soft searches” that don’t harm your record.(loanex.space)

- Diversify Credit Responsibly: A mix of credit types managed well shows risk handling.

Common Mistakes to Avoid

Even experienced Europeans make errors. Avoid:

- Ignoring your credit report

- Applying for too many products at once

- Letting bills go unpaid

- Assuming credit behavior in one country transfers to another

Remember: each country’s system is distinct — your good history in Germany won’t automatically help in France.(LegalClarity)

Comparing Credit Systems in Europe and the US

| Feature | Europe | United States |

|---|---|---|

| Unified Score | (Country‑specific) | ✔ Single model (FICO/Vantage) |

| Data Rights | GDPR protection | Fair Credit Reporting Act |

| Reporting Bias | Varies by nation | Standardized nationwide system |

| Impact on Lending | Lender discretion high | Score heavily influences decisions |

This comparison helps global readers understand the nuances and why European credit score tips must be region‑specific.

How European Credit Bureaus Assess Your Creditworthiness

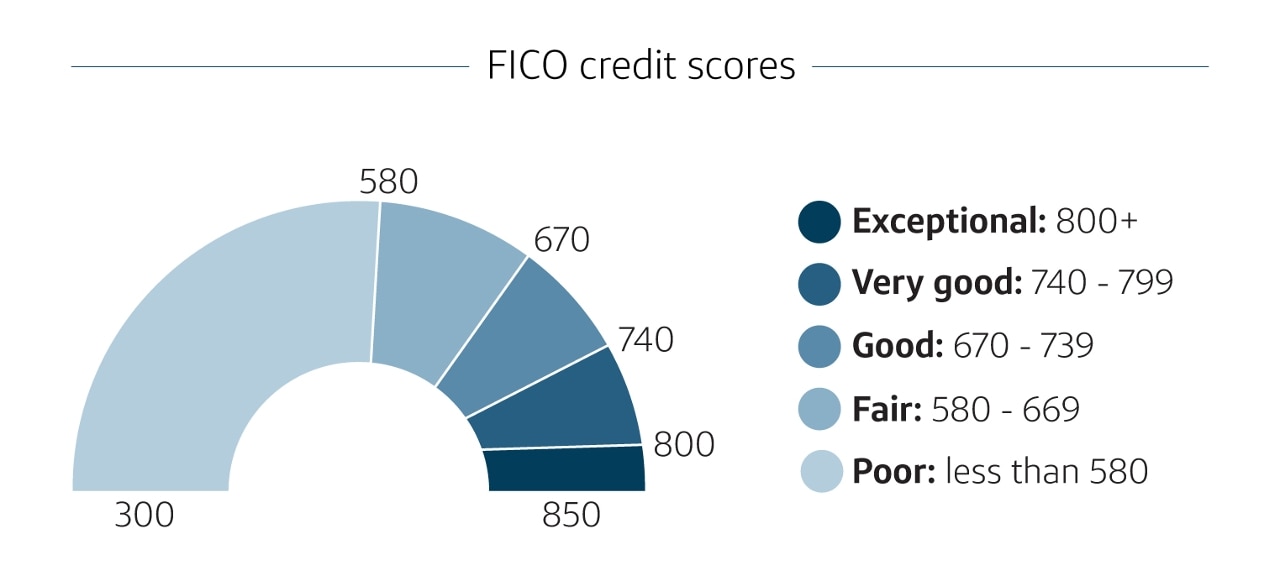

When thinking about credit score Europe, one of the first questions many people ask is: “Who actually calculates my credit score, and how do they determine my financial trustworthiness?” Unlike the United States, where the FICO or VantageScore is the standard, Europe has a fragmented credit reporting system, with each country operating its own bureaus and methodologies. Understanding how these bureaus work is a crucial first step in how to get a perfect credit score in Europe.

1. Country-Specific Credit Reporting Systems

European countries do not share a unified credit database. Here’s a brief overview of how some key nations handle credit reporting:

- Germany: SCHUFA

SCHUFA collects information from banks, utility companies, and financial institutions. Payment delays, outstanding debts, and credit applications are factored into your score. The score ranges from 0 to 100, with higher values indicating better creditworthiness. - United Kingdom: Experian, Equifax, TransUnion

The UK has three major bureaus, each maintaining a numerical credit score. Factors like payment history, outstanding debt, credit applications, and length of credit history determine your score. Tools like offer personalized guidance on improving your score. - France: Banque de France

Instead of a single numerical score, France maintains records of credit incidents such as defaults, late payments, or bankruptcies. Lenders refer to this registry when evaluating credit applications. - Spain, Italy, Netherlands

Similar to France, these countries rely more on negative listing systems combined with bank-specific assessments, meaning no standardized number exists, but responsible financial behavior still impacts lending decisions.

2. Key Factors Credit Bureaus Consider Across Europe

Although systems differ, most European bureaus assess similar factors to gauge your creditworthiness:

- Payment History – Are you consistently paying bills, loans, or credit card balances on time?

- Outstanding Debt Levels – High debt utilization may indicate risk, even without a numeric score.

- Length of Financial History – Older accounts demonstrate stability and reliability.

- Credit Applications – Multiple applications in a short period can be seen as risky behavior.

- Accuracy of Records – Errors or outdated information can unfairly lower your perceived trustworthiness.

Understanding these factors is essential for anyone seeking a perfect credit score in Europe. Even without a single number, your financial behavior is tracked and interpreted by lenders when approving loans, mortgages, or credit cards.

3. How Lenders Use This Information

European credit bureaus don’t just produce a number; they provide insightful reports that lenders analyze:

- Banks use this data to decide interest rates for loans or credit cards.

- Employers or landlords (in certain countries) may check credit behavior to assess financial reliability.

- Insurance companies sometimes factor in credit reliability when determining premiums.

This is why knowing how your behavior is viewed by these bureaus is crucial. Simple missteps, like missing a utility payment or leaving errors on your report, can directly affect your ability to access favorable financial products.

4. Practical Tips to Optimize Your Credit Report

- Request a free credit report at least once per year – most European countries allow this under GDPR.

- Check for errors and dispute them immediately – a single mistake could lower your credibility.

- Maintain long-term financial relationships – old accounts demonstrate stability.

- Limit credit applications – only apply when necessary to avoid raising red flags.

By actively managing your credit profile with these strategies, you’re already taking the first step in step by step credit score improvement Europe 2026.

Takeaway

Understanding how European credit bureaus assess your creditworthiness is the foundation for building a perfect credit score Europe. Once you know what they measure, you can adopt smart habits to influence these assessments positively — paving the way for better loan terms, lower interest rates, and greater financial freedoM.

Common Mistakes Europeans Make That Lower Their Credit Score

When aiming for a perfect credit score Europe, it’s not just about doing the right things—it’s also about avoiding the wrong ones. Many Europeans unknowingly make financial errors that can seriously damage their creditworthiness. Understanding these pitfalls is crucial for anyone seeking step by step credit score improvement Europe 2026.

1. Ignoring Your Credit Report

One of the most common mistakes is simply not checking your credit report. Even minor inaccuracies—like a misreported payment or outdated account information—can negatively affect how lenders perceive you.

Tips to avoid this:

- Request your credit report at least once per year. In most European countries, GDPR gives you the right to access your financial data for free.

- Look for incorrect debt listings, duplicate entries, or outdated addresses.

- Correct errors immediately by contacting the credit bureau.

Pro Tip: In Germany, you can request your SCHUFA report once per year for free. In the UK, all three major bureaus—Experian, Equifax, and TransUnion—offer free annual credit reports.

2. Missing Payments or Paying Late

Payment history is the single biggest factor affecting your credit standing across Europe. A single missed or late payment can stay on your record for years, affecting your ability to secure loans, mortgages, or credit cards.

Practical strategies:

- Set up automatic payments for recurring bills.

- Keep a calendar reminder for due dates to avoid late payments.

- Prioritize paying off credit cards or loans before the due date to maintain a clean record.

3. Overusing Credit or Maxing Out Accounts

Even if you’re making payments on time, high utilization of your credit lines can signal risk to lenders. Generally, keeping your utilization below 30% of your available credit is considered optimal.

Mistake examples:

- Maxing out multiple credit cards at once.

- Frequently borrowing large amounts without repaying quickly.

Tip: Spread your spending across multiple cards or accounts while keeping balances low to maintain a favorable profile.

4. Applying for Too Many Loans or Credit Cards at Once

Frequent credit applications are another common mistake. Each hard inquiry can signal financial stress and negatively affect your credit assessment—even if you’re ultimately approved.

Tips to manage this:

- Only apply for credit when necessary.

- Use soft inquiries when comparing offers—these don’t affect your credit report.

- Keep a long gap between applications for new credit products.

5. Ignoring Old Debts or Outstanding Accounts

Old debts or accounts with unpaid balances, even if minimal, can remain on your record and damage your creditworthiness. Some European countries maintain negative lists for defaults or late payments that can last for several years.

How to address this:

- Settle old debts as soon as possible.

- Negotiate payment plans with lenders to show good faith.

- Regularly check that cleared debts are updated on your report.

6. Failing to Diversify Credit Responsibly

While European lenders may not require a “mix” of credit types like the US, showing responsible use of different types of credit can strengthen your profile. Relying solely on one type of account, such as a single credit card, might limit your perceived reliability.

Suggested approach:

- Maintain a small loan or credit card responsibly.

- Consider using payment facilities that report on-time payments to the bureaus.

- Avoid overextending; diversification is about showing responsible use, not accumulating debt.

Quick Checklist: Mistakes to Avoid

- Ignoring your credit report

- Missing or late payments

- High credit utilization

- Multiple credit applications in a short time

- Leaving old debts unpaid

- Lack of credit diversification

By systematically addressing these errors, you not only improve your rating but also set yourself up for achieving a perfect credit score Europe.

Takeaway

Avoiding these common mistakes is just as important as following positive strategies. A clean, accurate, and well-managed credit profile is the backbone of step by step credit score improvement Europe 2026.

Remember: even small, consistent actions—like paying on time or correcting errors—can dramatically enhance your creditworthiness over time.

Advanced Credit Score Hacks for High-Income Earners in Europe

Achieving a perfect credit score Europe isn’t just for first-time credit users or average earners—it’s also essential for high-income individuals who want to leverage their financial power for better loans, investment opportunities, and premium financial products. While high earners may already have strong income statements, lenders still scrutinize behavior, debt management, and credit patterns before offering top-tier terms.

This section will explore proven hacks and strategies tailored to high-income Europeans looking to optimize their credit profiles in 2026-2027.

1. Strategic Credit Diversification

High-income earners often have access to multiple credit lines and financial products. Using them responsibly can enhance perceived creditworthiness:

- Mix of credit types: Use a combination of credit cards, personal loans, or mortgage products responsibly.

- Demonstrate timely payments: Even if income is high, missed payments can significantly impact your profile.

- Avoid overleveraging: Taking on excessive debt, even if manageable, may signal risk to lenders.

Pro Tip: Use small, manageable loans to show consistent, positive credit behavior without risking your liquidity.

2. Maximize Positive Reporting Across Platforms

Many European credit bureaus don’t automatically include all your financial behavior. High-income earners can actively ensure positive habits are recorded:

- Utility and subscription payments: Certain services now report timely payments to credit bureaus, improving your record.

- Regular savings and investment behavior: While not always counted in a score, some lenders consider stable, consistent financial activity as an indicator of reliability.

- Authorized user accounts: Being added to accounts with strong histories can subtly strengthen your profile.

3. Soft Credit Inquiries for Better Terms

Instead of repeatedly applying for loans or credit cards—which generate hard inquiries and reduce your creditworthiness—high-income individuals should:

- Use soft inquiries to compare products. These are visible only to you and don’t impact your credit score.

- Negotiate terms privately with banks, leveraging your strong income as a bargaining tool for lower interest rates.

Why it works: Lenders often consider high-income applicants low-risk, but too many visible applications can signal instability or high credit dependency. Soft inquiries keep your record clean.

4. Automate Payments and Track Utilization

Even high earners can slip into pitfalls of high credit utilization if spending grows rapidly. To maintain a perfect credit score:

- Set up automated payments for all credit lines.

- Keep credit utilization under 30% of your available credit.

- Track spending using apps or dashboards that consolidate all accounts in one view.

Insight: Automation ensures consistency—a key factor in European credit assessments.

5. Optimize Debt-to-Income Ratio for Lending Advantage

Even with strong income, lenders look at debt-to-income (DTI) ratio when approving large loans, mortgages, or investment credit:

- Maintain a DTI below 35% for optimal approval odds.

- Strategically pay down high-interest debts to free up borrowing power.

- Consider consolidating debts where possible for better long-term management.

6. Leverage Legal Rights Under GDPR

High-income earners often have more complex financial portfolios. Ensuring your credit report is accurate and updated is crucial:

- Request full annual reports from all relevant bureaus.

- Dispute outdated, inaccurate, or duplicated entries.

- Document your communications to ensure corrections are implemented promptly.

Pro Tip: Using your GDPR rights proactively can prevent small errors from impacting significant loan applications or credit lines.

7. Use Credit Strategically for Investments

High-income Europeans can enhance wealth growth while improving credit:

- Use low-interest loans or credit lines for investments where returns exceed borrowing costs.

- Maintain consistent repayment to demonstrate financial responsibility.

- Diversify portfolio risk without overleveraging—this signals financial acumen to lenders.

Quick Checklist: Advanced Credit Hacks

- Diversify credit types responsibly

- Ensure all positive behavior is reported

- Utilize soft inquiries for loan comparisons

- Automate payments and track credit utilization

- Maintain optimal debt-to-income ratio

- Correct errors using GDPR rights

- Use strategic borrowing for investments

Takeaway

High-income Europeans have unique opportunities to optimize credit beyond the basics. By combining strategic credit usage, positive reporting, and proactive management, you can achieve step by step credit score improvement Europe 2026, unlocking the best financial products, investment opportunities, and a strong, reliable financial reputation across Europe.

Tools and Resources to Track and Improve Your Credit Score Europe

Achieving a perfect credit score Europe requires more than just good financial habits—it also involves using the right tools and resources to track and improve your credit score Europe effectively. High-quality monitoring, smart budgeting, and reliable reporting are essential for step by step credit score improvement Europe 2026. In this section, we explore the most effective tools and resources Europeans can use to manage, optimize, and maintain a strong credit score Europe.

1. Credit Monitoring Platforms for Credit Score Europe

Using credit monitoring tools helps you track changes to your credit score Europe in real-time, alerting you to new activity, errors, or potential risks. Monitoring your score is critical for anyone who wants to improve credit rating efficiently.

| Platform | Country Coverage | Key Features | Do-Follow Link |

|---|---|---|---|

| Experian | UK, Ireland | Full credit report, alerts, score simulator, personalized tips for credit score Europe | |

| Equifax | UK, Europe | Credit report access, identity protection, alerts for changes, guidance to boost credit score Europe | |

| SCHUFA | Germany | Annual free credit report, score monitoring, correction requests for credit score Europe | |

| Creditsafe | EU-wide | Business and personal credit reporting, risk analysis, tools to track credit score Europe |

Pro Tip: Use these platforms to monitor all activity affecting your credit score Europe, including credit applications, inquiries, and balances.

2. Automated Payment and Budgeting Tools to Maintain Credit Score Europe

Automating payments is a cornerstone of step by step credit score improvement Europe 2026. Timely payments directly influence your credit score Europe, so using reliable budgeting tools ensures consistency:

- Mint – Tracks spending, sets reminders for bills, and helps maintain an optimal credit score Europe.

- YNAB (You Need A Budget) – Allocates funds efficiently to improve your credit rating and monitor your credit score Europe.

- Revolut/Monzo Banking Apps – Offer real-time alerts, scheduled payments, and balance tracking for maintaining a strong credit score Europe.

Consistent automation ensures your credit score Europe is positively impacted month after month.

3. Credit Report Dispute and Correction Services for Credit Score Europe

Errors on your credit report can damage your credit score Europe. Using formal dispute channels helps correct mistakes and ensures your credit rating accurately reflects your financial behavior:

- Experian Dispute Portal – Submit corrections to maintain an accurate credit score Europe.

- SCHUFA Correction Service (Germany) – Fix outdated or incorrect entries to protect your credit score Europe.

Checking your report regularly and disputing errors is a critical step in step by step credit score improvement Europe 2026.

4. Educational Resources and Expert Guides for Credit Score Europe

Learning how to optimize your credit score Europe is equally important as monitoring it. Trusted resources provide actionable guidance:

- MoneyHelper (UK) – Offers tutorials, tips, and insights to improve credit score Europe.

- LegalClarity.org – Explains European credit laws, reporting standards, and rights under GDPR to protect your credit score Europe.

Leveraging educational resources ensures you can track and improve your credit score Europe strategically.

5. Actionable Plan Using Tools for Credit Score Europe

- Sign up for at least one credit monitoring platform to track your credit score Europe.

- Automate all recurring payments to maintain a perfect credit score Europe.

- Regularly review reports and dispute errors to protect your credit score Europe.

- Use budgeting apps to manage finances and avoid negative impacts on credit score Europe.

- Combine insights from educational resources to optimize your step by step credit score improvement Europe 2026.

Takeaway

Using the right tools and resources is essential to achieving a perfect credit score Europe. By actively monitoring, correcting errors, automating payments, and learning from trusted sources, you can track and improve your credit score Europe effectively, ensuring your financial profile remains strong and attractive to lenders across Europe.

Conclusion: Achieve a Perfect Credit Score Europe in 2026‑2027

Achieving a perfect credit score Europe is not just about luck—it’s about understanding how European credit bureaus work, avoiding common mistakes, and applying step by step credit score improvement Europe 2026 strategies consistently. From monitoring your credit report to automating payments, leveraging advanced credit hacks, and using the best tools available, every action contributes to building a stronger financial profile.

High-income earners and everyday Europeans alike can benefit from these insights to improve credit rating, secure favorable loans, and access premium financial opportunities. By following these European credit score tips and staying disciplined, you can make measurable progress toward a perfect credit score Europe faster than you might expect.

Remember, a strong credit score Europe opens doors to better interest rates, smoother loan approvals, and financial confidence across the continent. Start today, track your improvements, and use the strategies outlined in this guide to ensure your credit score Europe reflects your true financial reliability.

With consistent effort and the right resources, achieving a perfect credit score Europe is entirely possible, and these steps will prepare you to navigate Europe’s financial landscape successfully through 2026 and beyond.

For deeper exploration:

- Learn about general credit improving strategies at Experian’s Official Guide on Credit Scores — a practical resource on what affects your credit and how to improve it.

- Check out the UK‑based MoneyHelper credit score advice for beginner tips and how credit reports work.

These reputable resources add credibility and depth to your credit knowledge.